Mind the tax authorities and treaties, but be mindful of "extra-taxation"

Hard-up governments can be creative in levying fees that others call taxes

I wrote recently about the need for emigrants to European countries to pay attention to the tax treaties with their home country. It’s essential, but it doesn’t capture the whole picture. Beyond income, inheritance and capital gains taxes there is a world of expenses such as fees for this or that government service. Think of fees for drivers’ licences, for example. And sometimes a government can resort to “levies” or other mechanisms to increase tax revenue. Some of these mechanisms move toward or into the domain of “extra-taxation.”

To get a fuller view of tax burden within a specific jurisdiction, one needs to understand all types of revenue against which a government will levy a claim, apart from taxes on income, capital gains and inheritance—especially if you move to a new country with intentions to work there.

European countries typically levy “social charges” on those who earn income within their jurisdiction. These are similar to the FICA charges that one pays in the United States, and their purpose is similar. They fund the social welfare system that serves qualified residents by providing healthcare services and retirement pensions, for example. These are not general considered taxes per se.

But there is also the phenomenon of extra-taxation: mandatory charges that lie beyond the formal tax framework which apply to individuals and/or organisations. Think of things like temporary levies and surcharges.

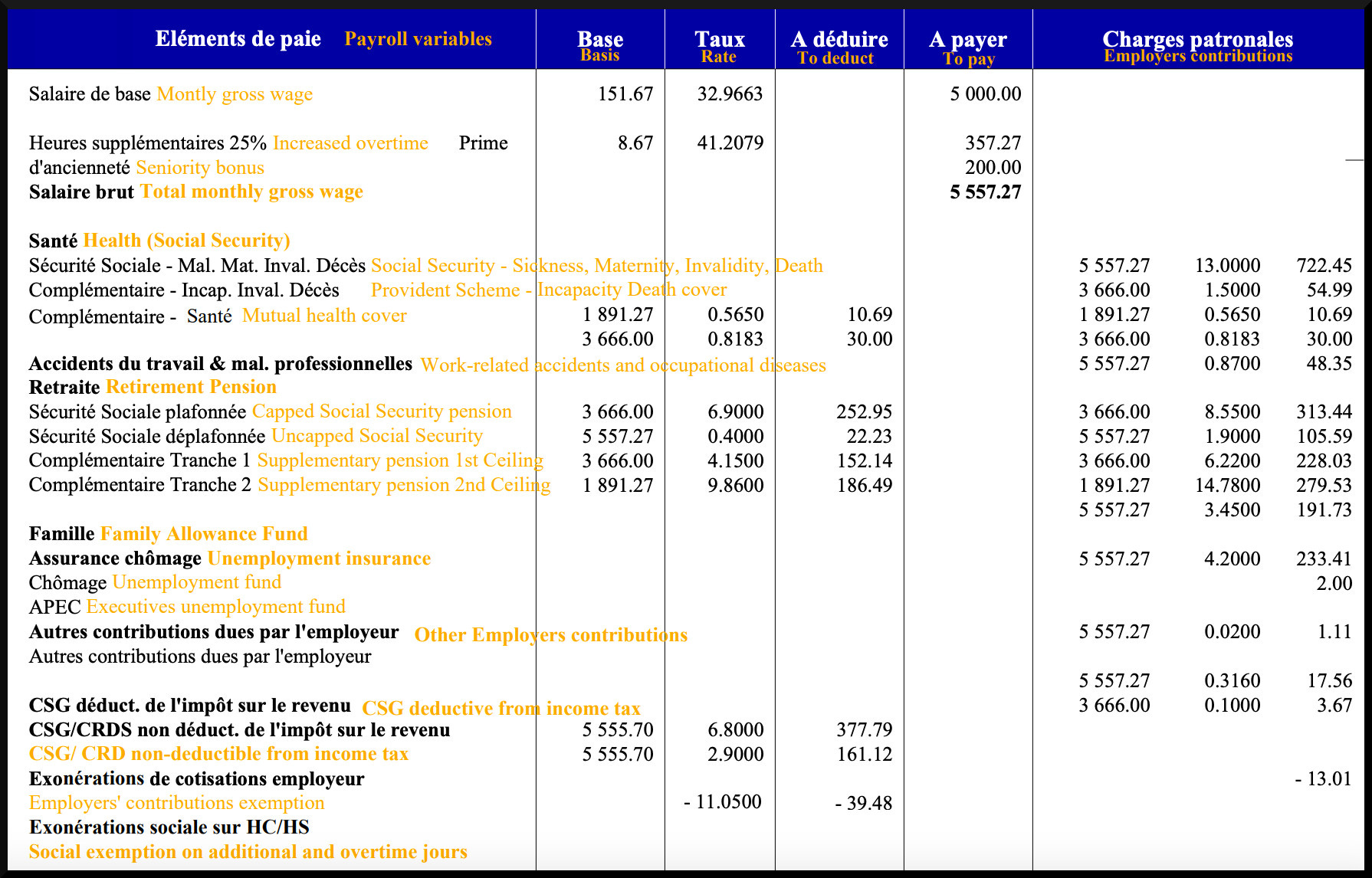

France, in particular, has been accused of avoiding conflicts with European Union guidelines on income taxation by increasing government revenue through two types of extra-taxation: the CSG (contribution sociale généralisée, or generalised social contribution) and the CRDS (contribution au remboursement de la dette sociale, or contribution to the repayment of social debt). Both types of charges apply to individuals who work in France and to French-sourced revenue under certain conditions. The service-public.fr website describes them as follows:

[Elles] sont prélevées sur les revenus d'activité (salaire, revenus des indépendants, etc.) et sur les revenus de remplacement (indemnités de chômage, pensions de retraite, etc.). Les taux varient selon les situations. Une partie de la CSG est parfois déductible pour l'impôt sur le revenu. Certains revenus sont exonérés de CSG.

[They] are levied on earned income (salary, self-employed income, etc.) and on replacement income (unemployment benefits, retirement pensions, etc.). Rates vary depending on the situation. A portion of the CSG is sometimes deductible from income tax. Certain types of income are exempt from CSG.

These charges are levied on individuals who are fiscally resident in France and who benefit from a compulsory French health insurance scheme. Both conditions must apply.

American emigrés to France should understand that these charges apply to their earned income from remote work for a non-French employer if they are beneficiaries of any state healthcare scheme, such as the PUMA (Protection Universelle Maladie, or Universal Health Protection); they also apply if an individual is a registered micro-entrepreneur generating revenue from work done in France. In addition, the charges apply to other forms of revenue—capital gains, rental income and dividends/income from investments. U.S. Social Security income is exempted. If, like me, you have worked and paid social charges in another E.U. country, the E.U. Court of Justice has ruled that CSG charges cannot be applied to foreign state pension income, as it would, in effect, be a form of double taxation. The topic is complex and further details are available at the economie.gouv.fr website.

So why do these French social charges come up when discussing extra-taxation? It is because in 2000, the Conseil constitutionnel (constitutional council) ruled that revenue from the CSG does not apply exclusively to future state benefits (such as healthcare and pensions) and therefore should be considered, from a legal perspective, a tax.1

France also has the Forfait social (social contract). This is a scheme that applies only to employers with more than 50 employees. Since this will apply to only a certain limited group of emigrés who start businesses, I leave it to the reader to investigate employers’ obligations at https://entreprendre.service-public.fr/. (The forfait social is charged according to employees’ pay, and for that reason is often considered a form of extra-taxation.)

France is not the only country where governments increase revenue through extra-taxation schemes. In general, instances of extra-taxation tend to be manifestations of “solidarity taxes,” where exceptional taxes are applied to certain cohorts for a period of time in order to promote fairness and equitable sharing of national expenditures across all levels of society. An example can be found in Germany, which instituted a Solidaritätszuschlag (solidarity surcharge) on income tax in 1991 to fund German reunification, which continues to apply to certain high earners. And Spain maintains a temporary Renta de Solidaridad (solidarity income), essentially a wealth tax applicable to high-net-worth individuals.

There have also been relatively recent instances of exceptional levies being applied on individuals and businesses during times of crisis, namely, the 2007-2009 financial crisis or “great recession.” Best known are those applied in conjunction with the financial “bailouts” made to Greece, Ireland, Portugal and Spain at the time. While the specific shape of the extra-taxation packages differed in each jurisdiction, these four countries shared a common burden of reduced income and restricted access to both private and public funding for the duration of the crisis.

My own experience in the Irish public sector at the time was a series of pay reductions consisting of pension levies and temporary reductions in pay. Restorations of pay were made after 2020 and 2021 (with corresponding adjustments to pensions for those who had retired during this period). However, the pension levy has never completely disappeared. Instead it morphed into a smaller, permanent levy on pensions called an Additional Superannuation Contribution (ASC)—a classic example of extra-taxation.

Another, more obscure detail of extra-taxation in Ireland is worth mentioning. If you are an Irish resident with an Irish bank account, and you leave Ireland to become tax resident in some other jurisdiction, any remittances that have been sourced from outside of Ireland (for example, U.S. Social Security payments) and that are deposited to your Irish bank account are considered taxable income by Irish Revenue. This rule applies for a period of three years after you have become tax-resident elsewhere. But, you say, it’s already been taxed in another country! Isn’t that double taxation? Sorry, this is a loophole that somehow lies beyond the terms of the tax treaty. Also sprach Irish Revenue. It’s the kind of thing you don’t find out about until it rises up and looks you in the eye.

The lesson here is that studying the tax treaties and the up-to-date national tax code might not show all the nasty details that lurk behind the scenes. Nearly all European countries have issues with a gap between revenue and government annual expenditures and they seek such “mechanisms” to try to mitigate financial shortfalls. Many agree that the existing imbalances of revenue and expenditure can be attributed to politically sensitive issues relating to social welfare policies and programmes. But these days those imbalances are aggravated by the uncertainty of American tariffs, the unreliability of the United States as a partner in Europe’s defence, and European support of Ukraine in its war with the Russian Federation. So don’t imagine they’ll be disappearing anytime soon.

There’s no realistic way to predict the future of individuals’ tax burden in Europe, but it might at least be useful to know it’s not just about what’s covered in the tax treaties and the national tax code of the country in which you choose to reside.

If you found this useful, please feel free to …

Conseil constitutionnel, “Décision n° 2000-437 DC du 19 décembre 2000: Loi de financement de la sécurité sociale pour 2001,” https://www.conseil-constitutionnel.fr/decision/2000/2000437DC.htm (consulted 29 June 2025)

This is so clear and well researched, thank you.

There are two things that get in my craw:

1.) Social media nonsense that tells people healthcare and such here are free. We pay big taxes for the services.

2.) Social media and Facebook nonsense talking about “remote work.” “Remote work” is a gray area. And if your tush is in a chair in France, you probably owe French taxes.

This Substack is a wealth of information.

One of the reasons a relative gave up her US citizenship after decades in Canada was US taxes. The relative wanted to sell her house, and apparently the capital gains are taxable in the US. This would also apply if her child, also a US citizen, was to inherit the house and sell it. My relative is a lawyer and consulted other lawyers about this, and decided the simplest thing was to renounce.